Every major platform has moved into ecommerce. Google has Shopping. Instagram, TikTok, and Facebook have native checkout. And now ChatGPT is offering to sell you things directly, no brand website required.

The question brands are quietly panicking about: if platforms become the place where purchases happen, what’s left for brand websites to do?

We surveyed 49 shoppers to find out how they actually feel about buying through platforms versus buying directly from brands. The results were more complicated than we expected. Many people are aware of in-platform shopping. Most are uncomfortable with it. And the most immovable resisters are not who you’d think.

In Our Survey, Here’s What Stood Out

- Awareness isn’t the problem. 81% of respondents knew in-platform shopping existed. Only 27% have ever actually done it.

- The brand website is holding its ground. 80% of shoppers trust and prefer brand websites more than platforms, and that level of preference hasn’t weakened over the past year.

- Comfort level is the real barrier. 71% of shoppers are uncomfortable with in-platform purchasing to some degree.

- One purchase changes everything. Shoppers who have bought in-platform once are significantly more open to doing it again, and feel more positively about every platform, including ones they haven’t bought on yet.

- The most resistant shoppers aren’t technophobes. 96% of respondents are at least moderately tech-savvy. Resistance is informed, not fearful, and for some, it’s a deliberate choice.

- Men and women are having completely different experiences. Women are three times more likely than men to have bought in-platform. But they use different platforms, have different concerns, and respond to different things.

- ChatGPT has the furthest to go. 70% of respondents are negative about shopping through ChatGPT (the highest of any platform we asked about). But among those who have bought in-platform before, nearly half are open to trying it.

Our Survey Methodology

This survey was conducted with 49 respondents across our network.

Participants were asked 22 questions covering their:

- Awareness of in-platform shopping features

- Comfort levels and concerns

- Preferences and behaviours

We focused our survey on Google, ChatGPT, and social media platforms with shoppable features (Instagram, Facebook, TikTok, and Pinterest). When we mention “in-platform” purchases, we mean purchases made directly on these platforms, without visiting a brand’s website.

The sample of participants skews toward digitally active, mid-career shoppers. For instance,

- 60% of respondents are aged 35–54

- 88% shop online at least a few times per month

- 96% describe themselves as at least moderately comfortable with technology

The gender split is roughly balanced: 49% female, 43% male, with the remainder preferring not to say or remaining undisclosed.

Because of the sample size, findings are directional rather than statistically definitive. They reflect the views of an engaged, digitally fluent audience, which means resistance to in-platform shopping in this group is arguably more considered than you’d find in a broader population sample.

Where patterns are strong and consistent across multiple questions, we’ve treated them as meaningful insights. Where sample sizes within subgroups get small, we’ve treated findings as directional only.

All percentages are rounded to the nearest whole number. Open-text responses and quotes from participants have occasionally been lightly edited for spelling and brevity only.

Here are our findings.

1. Shoppers Still Trust Brand Websites, But It’s Not Unconditional

If platforms are hoping shoppers will abandon brand websites in favor of buying directly where they discover products, the data suggests they’ll be waiting a while.

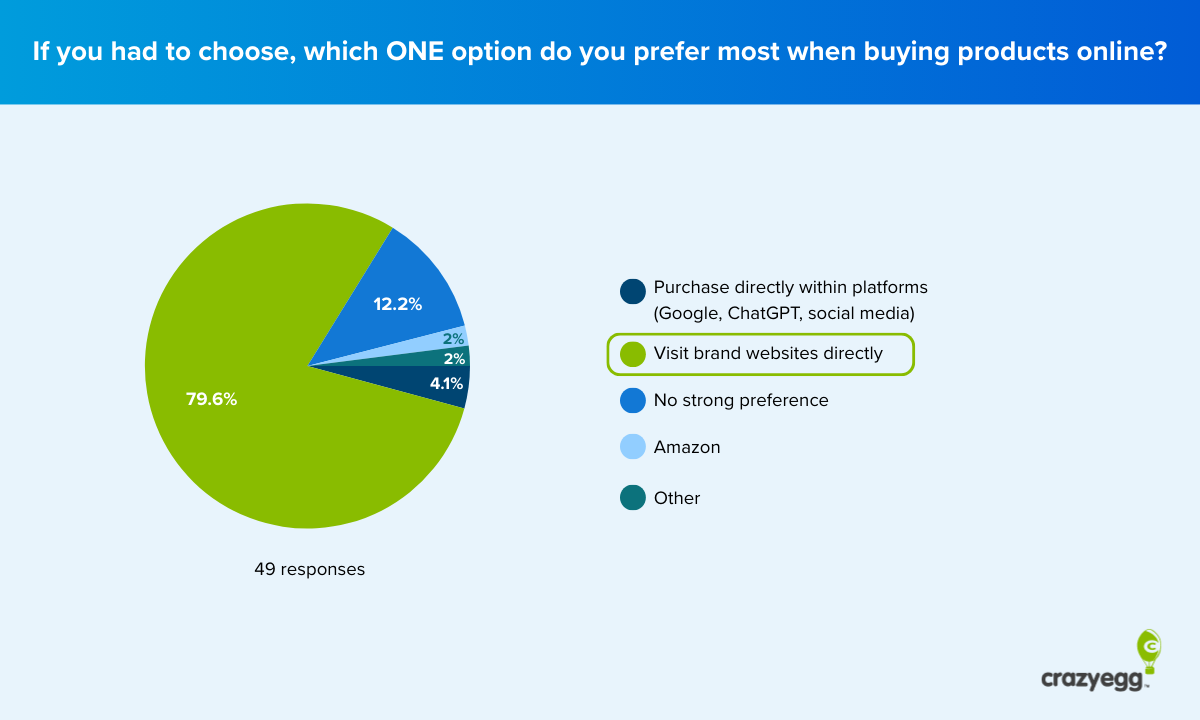

80% of respondents said their preferred destination for completing a purchase is the brand’s website.

Only 4% said they’d choose to buy within the platform where they found the product. And when asked whether their brand website usage had changed over the past year, 69% said it was about the same (with 20% actually increasing how often they visit brand sites).

That’s not a channel in decline. That’s a channel with a firm hold on consumer preference.

But dig into the reasons why, and a more complicated picture emerges. Trust and security are dominant themes, but so is scepticism about everything else. Shoppers aren’t just choosing brand websites because they love them. They’re choosing them because they don’t yet trust the alternatives.

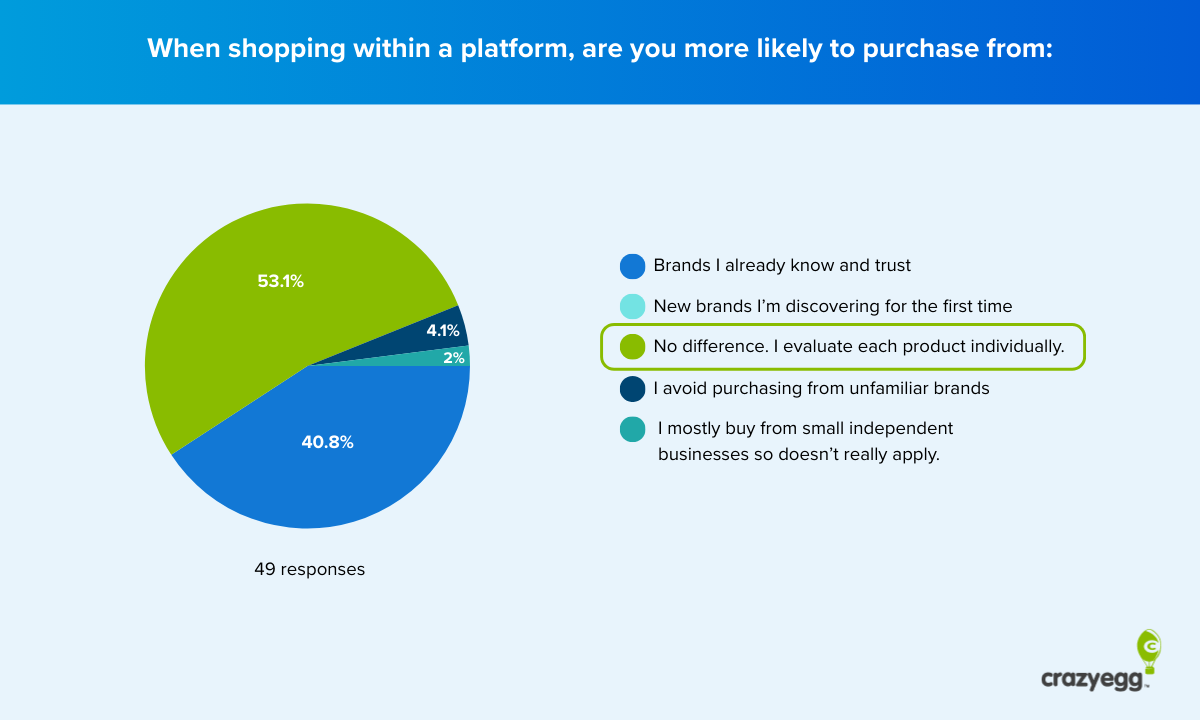

For instance, more people prefer to evaluate each product individually, regardless of whether it comes from a brand they know and trust.

The main concerns that lead to consumers buying direct from brands cluster around a few consistent themes:

- Avoiding scams

- Accessing better product information

- Keeping their data out of platform ecosystems

- Wariness of algorithms pushing products based on commission rather than quality

As evidenced by open-answer responses like these:

“I prefer avoiding intermediaries, especially ones that push content and products based on shady algorithms.”

“I will actively close Instagram, even if I see something I want to buy. I will Google search the product to look for it at a .com.”

That second quote is worth sitting with. This respondent has actually made in-platform purchases before, and she still goes out of her way to avoid completing them. The resistance isn’t always about inexperience. For many shoppers, it’s a deliberate, eyes-open choice.

The brand connection question

Beyond trust and security, there’s an emotional dimension that surprised us.

59% of respondents said they feel more connected to a brand when buying directly from its website rather than through a platform (even the brand’s official social channels). For many shoppers, where they buy is part of how they relate to a brand, not just a logistical detail.

That feeling is strongest among those who haven’t bought in-platform yet, as 69% feel more connected when buying direct. Among those who have made an in-platform purchase, that drops to 30%, with 62% saying the channel makes no difference to how they feel about the brand at all.

It’s not just that experienced in-platform shoppers feel less connected when buying direct, they’ve largely stopped associating the brand relationship with the channel altogether.

The value question is less clear-cut

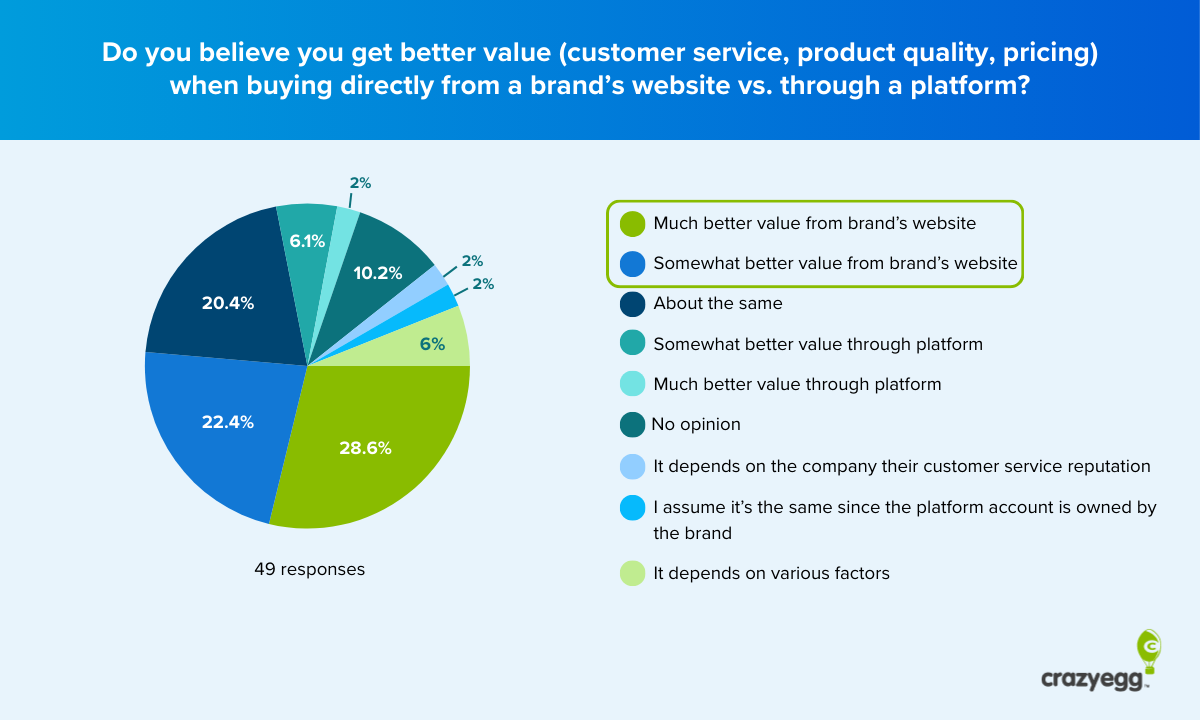

Trust leans heavily toward brand websites. But value? Less so.

51% of respondents believe they get better value from a brand’s website, a volatile majority.

The open text responses captured this tension well:

“Brand websites strike me as more reliable but frequently don’t have the product deals of a platform or marketplace.”

“MSRP is almost always higher when you visit a brand website, so if the brand had the item for sale at the discounted price, I would likely buy it directly from them.”

The implication for brands is clear: trust and reliability are largely won. Value and price competitiveness are not.

Shoppers who prefer buying direct are often doing so despite feeling they might be paying more, not because they’re convinced they’re getting the best deal.

The good news for brands comes with a caveat

Brand websites aren’t losing the preference battle. But the loyalty they enjoy is partly defensive and built on distrust of platforms rather than unconditional affection for the direct channel. That’s a more fragile position than the numbers suggest.

If platforms get meaningfully better at addressing the trust and security concerns that currently drive shoppers back to brand websites, the preference gap could close faster than brands expect.

The good news: 20% of shoppers are actively increasing their brand website usage. The direct channel has genuine momentum among a portion of the audience. The challenge is making sure that momentum is based on what brand websites do well, not just on what platforms haven’t yet earned.

2. Shoppers Know the Platforms, But Most Just Aren’t Buying There

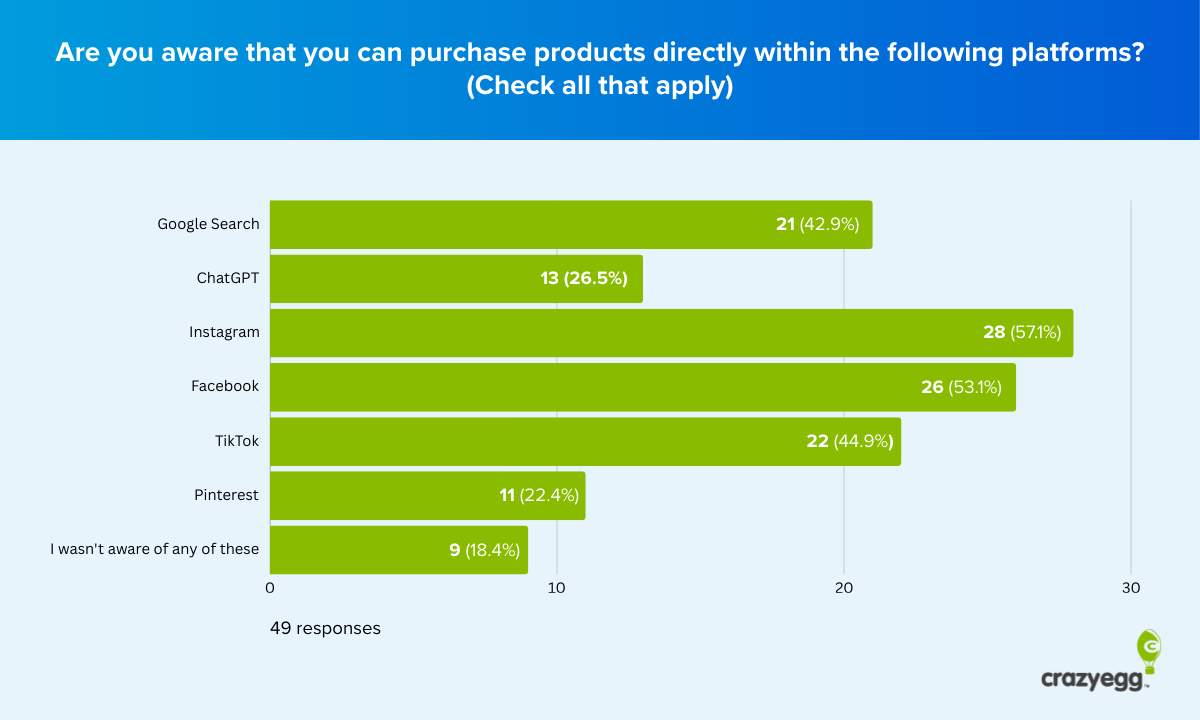

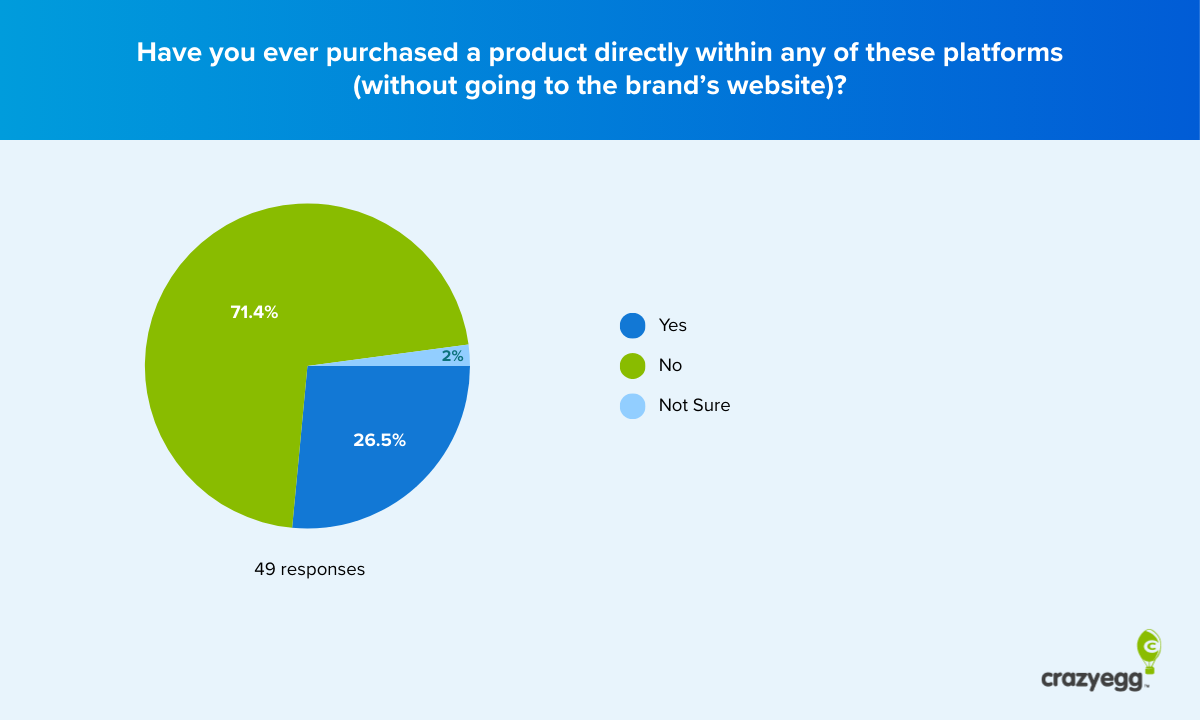

40 out of 49 respondents knew they could buy directly through at least one of the platforms we asked about.

Only 13 have ever actually done it.

Awareness of in-platform shopping is very high in this sample. Converting that awareness into a purchase is where things fall apart.

71% are uncomfortable with in-platform purchasing to some degree. 84% made zero in-platform purchases in the past three months. And when asked what their preferred channel is, 80% still point to brand websites.

Here’s how each platform is landing with shoppers right now.

Google Search

Google has the most familiar brand of any platform we tested, and it shows. It’s the least negatively rated of the three, with 38% feeling negatively and 20% positively.

But familiarity hasn’t translated to purchases. Only 4 of the 21 respondents aware of Google Shopping have actually bought there

One response captured an interesting insight: “I confidently purchase flights on Google, but no products that I can think of.”

Google has earned category-specific trust in industries like travel, but not for general ecommerce.

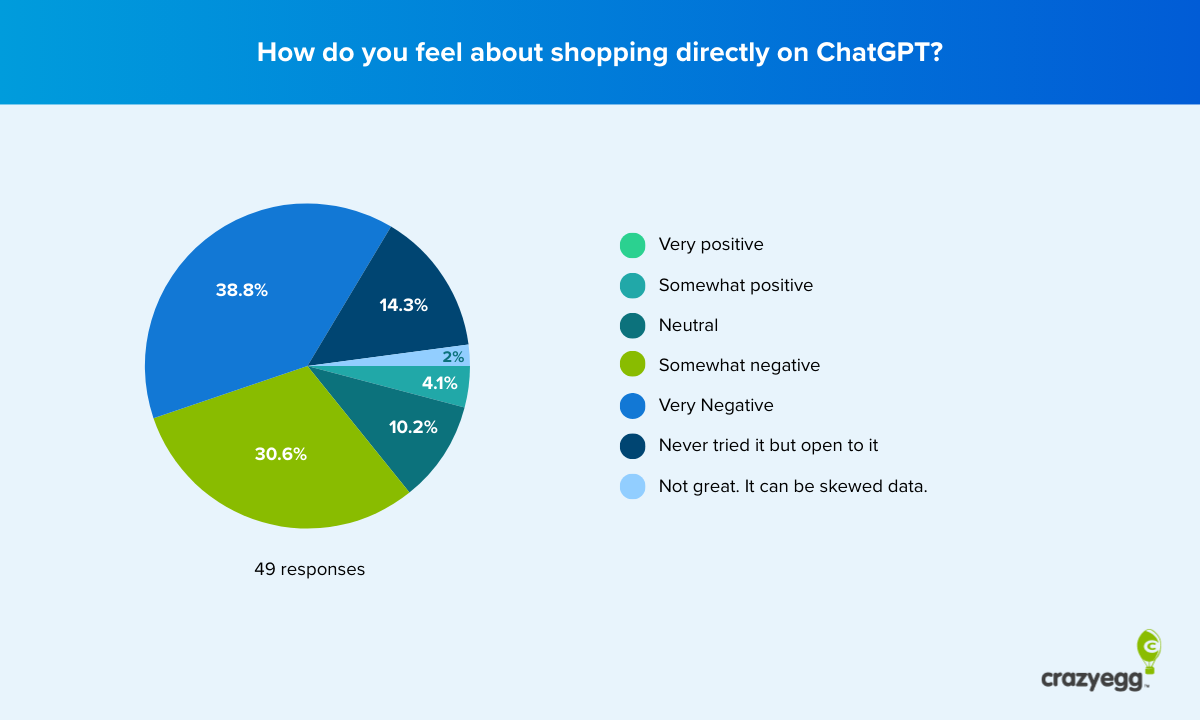

ChatGPT and AI

ChatGPT is the hardest platform to shift sentiment on. 70% of respondents feel negatively about shopping through it, the highest of any platform we asked about.

Only 4% are somewhat positive. And awareness is the lowest of all platforms tested, with only 13 of 49 respondents knowing it was even an option.

The resistance isn’t coming from people who don’t understand AI. Instead, it’s coming from people who understand it very well, as captured in this participant’s comments:

“I honestly think, because I’m so deeply familiar with how these platforms work… that I’m less likely to shop there. I don’t want the data sharing, I don’t want the influence from algorithms guiding my purchases.”

And in many cases, it’s not just a blanket rejection of the technology itself; it’s a more specific objection to how AI commerce is being monetized. One respondent drew a clear line between the concept and the commercial reality:

“I don’t care about where I buy. I think having an LLM suggest a product might be worthwhile, although I wouldn’t trust suggestions coming from ChatGPT, as that may likely be swayed by who is paying a higher commission.”

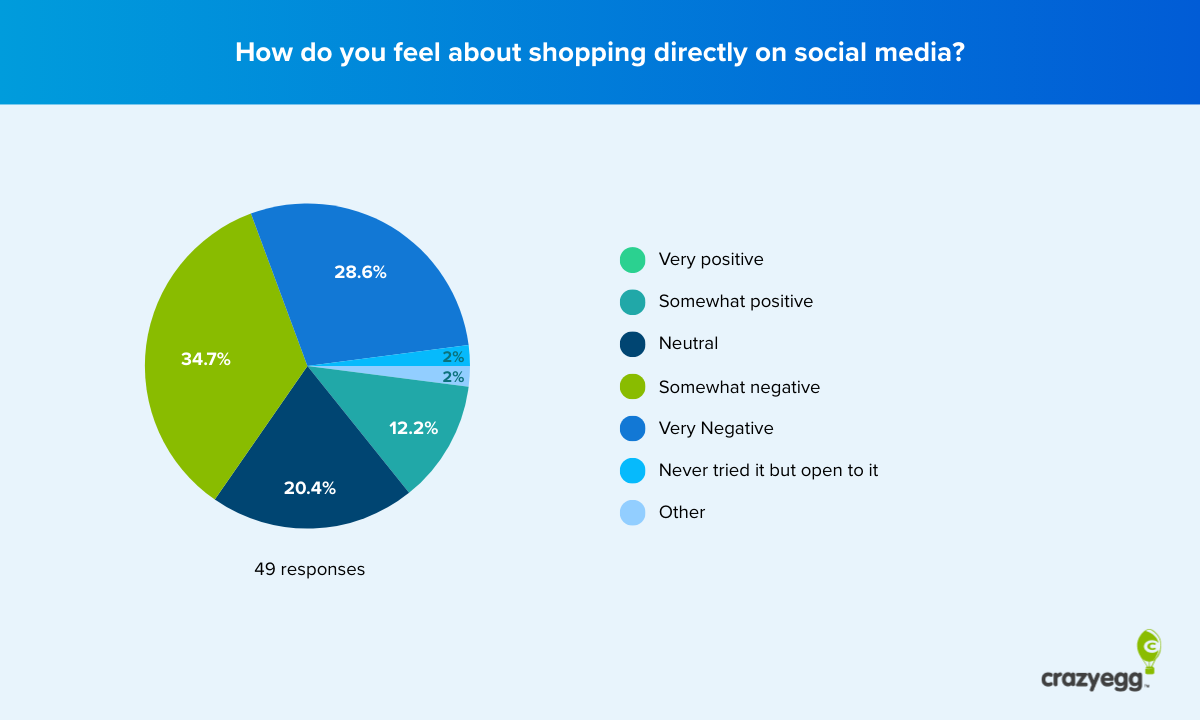

Social Media

Social media platforms sit in the middle: more trusted than ChatGPT, less trusted than Google. 64% of participants feel negatively about buying on social media platforms, but it’s also the option with the most room to move.

One response captured the dynamic well when asked how they felt about shopping directly on social media:

“Used to be negative, but recently got into Instagram and have to admit I have made a couple of purchases based off ads there.”

Sentiment on social commerce shifts with experience more than on any other platform. The challenge is getting people to that first experience.

A quick word on Amazon, eBay, and marketplaces

We deliberately excluded established marketplaces from this study.

Our focus was on platforms that built their audiences around content, search, or conversation — the places where product discovery tends to happen.

We limited the study to discovery platforms that are also expanding into commerce as a revenue stream. That’s a fundamentally different proposition from a platform people already visit to shop.

That said, Amazon and eBay came up repeatedly in open text responses, not as shopping destinations people love, but as a default they trust by familiarity. As one respondent put it: “At least Amazon is the evil I know.”

Amazon’s returns, customer service, and price comparison consistently came up as the reasons people reach for it by default instead of shopping in-platform or through a brand’s website.

“I am a Prime member, so knowing I can easily return a product gives me some assurance.”

That framing matters for understanding in-platform resistance more broadly.

For many shoppers (particularly men and older age groups), the competition for the purchase isn’t between brand websites and platforms. It’s between brand websites and Amazon. New platforms asking for that transaction are competing against a default that took years and billions of dollars to build.

3. How People Actually Shop Online And Where Platforms Fit In

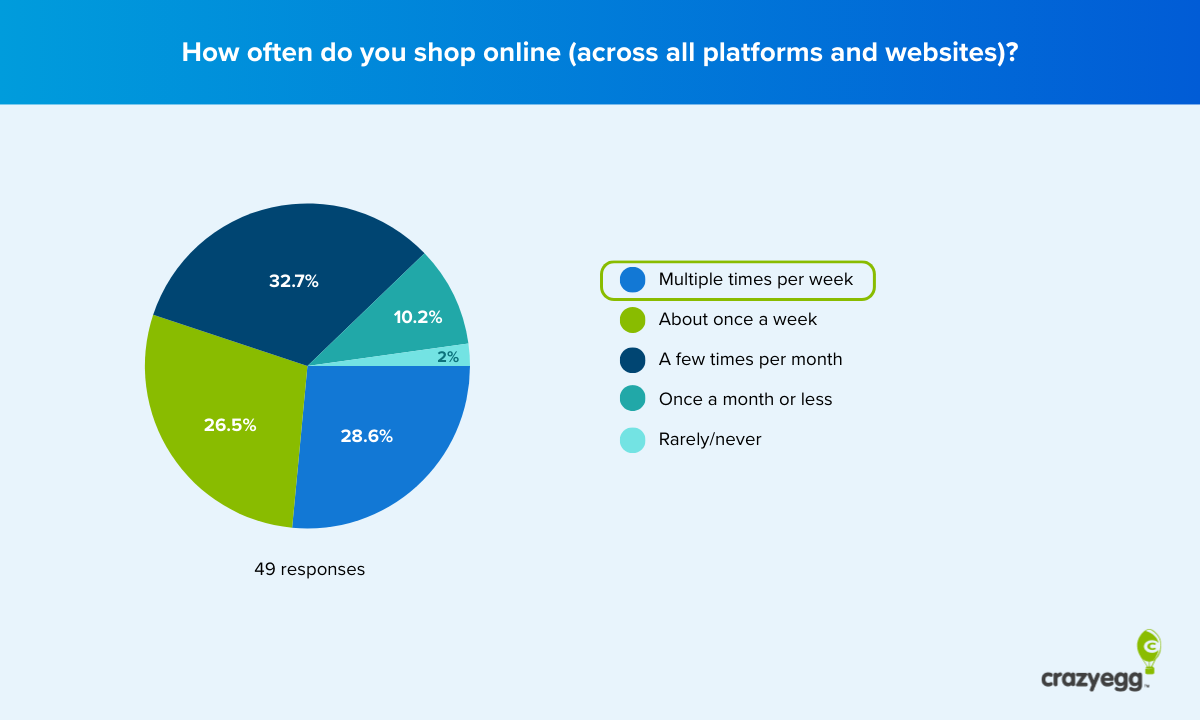

The shoppers in this study are not occasional browsers. 89% shop online at least a few times per month, with 29% doing so multiple times per week.

This is an active, digitally fluent sample, which makes their resistance to in-platform purchasing harder to dismiss as unfamiliarity or inertia.

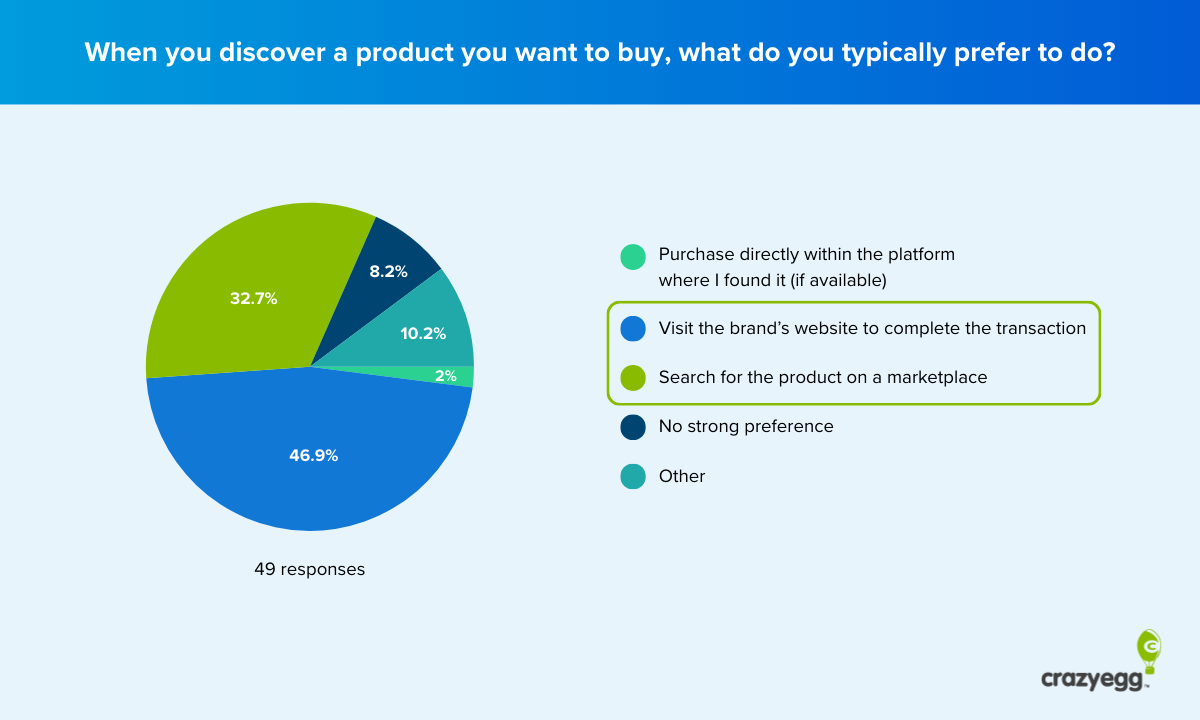

When they discover a product they want to buy, most follow a well-worn path.

- 47% go directly to the brand’s website

- 33% head to a marketplace like Amazon

- Only 1 in 49 completed the purchase within the platform they found it

That default behaviour is also remarkably stable. 69% say their brand website usage hasn’t changed in the past year. And shopping frequency doesn’t predict openness to new channels. People who have not bought on a platform shop online marginally more often than those who have bought on a platform.

Shopping more online doesn’t appear to make you more willing to do it differently.

What does predict channel choice, it turns out, is how comfortable you are with the idea and whether you’ve ever crossed the line once before.

Both of those threads run through everything that follows.

4. Men and Women Shop Online Very Differently

The gender split in this data is one of the most consistent findings across the entire survey, and it runs deeper than purchase rates.

Women are three times more likely to have bought in-platform than men (42% vs 14%), and account for 77% of all in-platform buyers despite making up 49% of the sample.

And yet women also have the strongest brand website preference of any group. 92% say it’s still their preferred destination. The paradox: the most active in-platform buyers are also the most committed to brand websites.

For some, the distinction between channels may not feel like a contradiction at all:

“I think social media is different since it’s owned by the brand. Google and ChatGPT feel less secure.”

When a brand’s official Instagram account is perceived as an extension of the brand itself, buying there doesn’t feel like going through a middleman. It feels like going direct.

Behaviour and stated preference are more at odds for women than for any other demographic in this study.

When women do buy in-platform, it’s almost exclusively through social media (Instagram in particular). 80% of female buyers made their in-platform purchase there.

This is consistent with broader platform demographics; Instagram and TikTok skew heavily female in both usage and engagement, which may partly explain why social commerce has gained more traction with women than any other channel or demographic group.

The default channels tell a different story by gender, too. Men reach for Amazon first (52%), which explains much of their in-platform resistance; their alternative to brand websites isn’t platforms, it’s a marketplace they already trust. But when not buying on social media, women go to brand websites first (62%).

Their concerns are different too.

Women’s #1 worry is product authenticity, especially the fear of fakes and scams. Men’s concerns are more systemic. 71% worry about payment security, but equally as many worry that platforms recommend products based on commission rather than quality.

Men fear rigged recommendations. Women fear fake products. Two different types of distrust that require different reassurances and platform strategies to address.

5. Every Age Group Has a Different Relationship With In-Platform Shopping

If you expected age to produce a simple pattern like younger shoppers being more open and older shoppers being more resistant, the data has other ideas.

25-34

The youngest cohort in our sample is somewhat paradoxically:

- The most aware that buying in-platform is an option

- Tied for the highest in-platform purchase rate

- But also the most uncomfortable with buying in-platform

87% are uncomfortable with in-platform purchasing to some degree, yet 50% have bought in-platform at least once. Their concerns focus on data privacy (88%) and pricing transparency (88%), the highest of any age group.

Brand website preference is unanimous: 100% say it’s still their preferred destination. Behaviour and stated preference are in direct conflict for this group more than any other.

35-44

This cohort is the most resistant to shopping directly within a platform in our study. Only 14% have bought in-platform, the lowest purchase rate among active buying age groups.

They have the strongest brand connection (71% feel more connected buying direct), the highest absolute trust in brand websites, and the most ethically motivated resistance to buying in-platform.

Their open-text responses contained the most value-based objections of any age group:

Algorithmic manipulation: “I prefer avoiding intermediaries, especially ones that push content and products based on shady algorithms.”

“I feel that Google, ChatGPT, social media, etc. all use the data to skew your results and target you with certain ads. I would rather keep that data separate.”

Ethical concerns about platform consolidation: “I love tech, I work with and in tech, but I loathe the use the tech oligarchs have been and are making of potentially beneficial systems for the exclusive goal of making themselves and shareholders richer.”

“I think AI was pushed public before it was ready and those that own AI are desperate to find ways to make it more financially viable.”

45-54

This is the counterintuitive one. Conventional wisdom would place 45–54-year-olds among the more cautious digital adopters. The data disagrees.

They’re tied with 25–34 for the highest in-platform purchase rate at 40%. Their defining concern isn’t trust or data privacy, it’s what happens after the purchase.

Returns difficulty leads at 73%, the highest of any age group, consistent with a cohort that has built strong loyalty to Amazon’s fast delivery and post-purchase support infrastructure. If platforms want to convert 45–54-year-old shoppers, matching Amazon’s customer experience and returns policy may matter more than anything else.

55-64

Moderate resistance, moderate awareness, and the most channel-agnostic group in the study. Only 50% strongly prefer brand websites, the lowest of any age group. Amazon is the dominant default (50%).

Their concerns are practical rather than principled, making them theoretically more convertible than their low purchase rate (17%) suggests.

65+

This age group had zero in-platform purchases in our sample, 67% default to Amazon, and there’s unanimous brand website trust. The resistance here is habitual rather than hostile and built on familiarity and post-purchase certainty rather than ideological objection.

6. Tech Fluency Doesn’t Predict Whether You’ll Buy In-Platform, But It Predicts How Strongly You’ll Feel About It

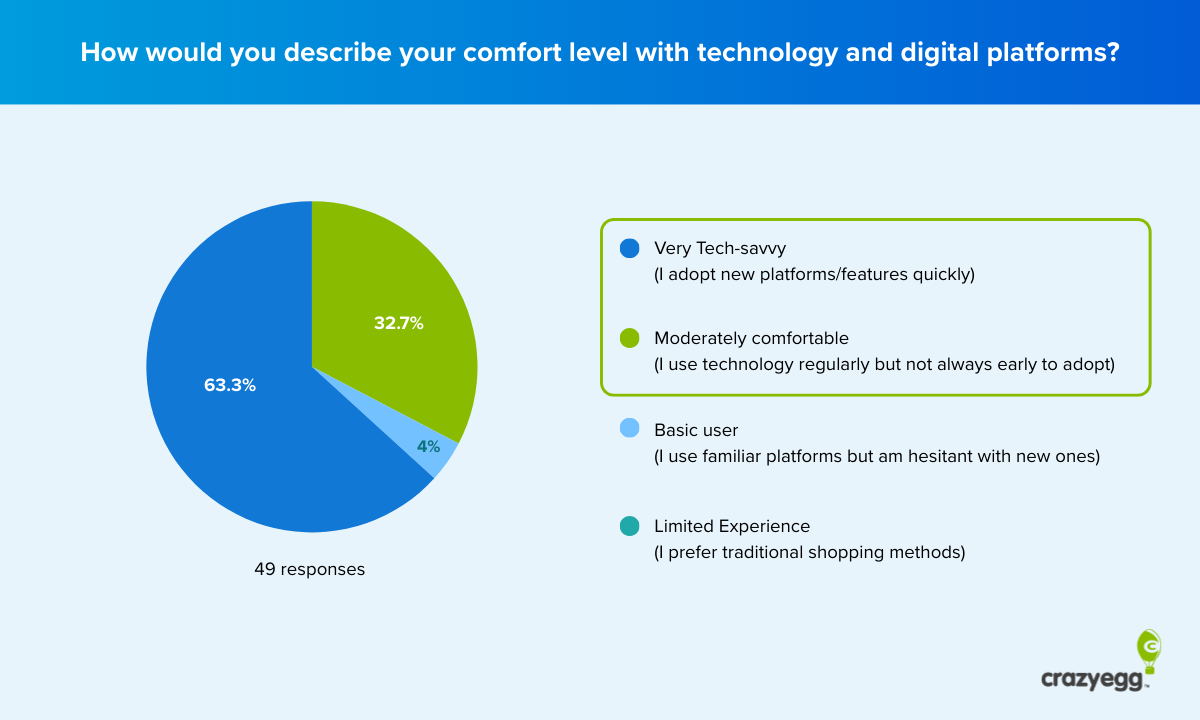

The first assumption this data circumvents is that resistance to in-platform shopping is driven by technophobia.

96% of respondents describe themselves as at least moderately comfortable with technology. 63% are self-described early adopters. This is not a sample of people who are scared of new things.

And yet the purchase rate among very tech-savvy respondents is 26%, virtually identical to the 25% rate among moderately comfortable users. Tech fluency and new platform adoption have almost no bearing on whether someone has bought in-platform. What it does affect is how strongly they feel about it.

Among moderately comfortable tech users, no one described themselves as comfortable with in-platform purchasing. They all sit in the uncomfortable-to-neutral range, with the majority (62%) landing at “somewhat uncomfortable.” There’s no one in this group who has crossed into feeling at ease with it.

Very tech-savvy respondents are significantly more likely to flag platform commission bias (58%) than moderately comfortable users (44%). The worry that platforms are manipulating recommendations for commercial gain isn’t a surface-level fear; it’s a knowledge-based one.

The people who understand how recommendation algorithms work are the most suspicious of them.

The “hard-no” segment

Within the very tech-savvy group sits a smaller but important subset: 10 respondents who said nothing would change their mind about buying in-platform.

Every single one is very tech-savvy. None has ever bought in-platform. And they’re distributed across ages 35–65, indicating that this is not a generational cluster. It’s a values-driven one.

These are not technophobes. They are informed, principled objectors who understand exactly what they’re resisting. No amount of UX improvement, faster checkout, or better pricing will reach this group. Their resistance is ideological, not practical — and the platforms’ own behaviour, from dynamic pricing to opaque algorithms and data harvesting, has arguably made it worse over time.

By comparison, only one respondent has actively embraced in-platform shopping and made over 10 purchases.

This goes to show how knowing more about modern technology doesn’t necessarily make people more likely to shop within emerging platforms. It makes their positions more fixed in polarizing directions.

7. What Separates the Shoppers Who’ve Crossed the Line From Those Who Haven’t

27% of respondents have made at least one in-platform purchase.

That’s a meaningful minority for this study. But what’s more interesting than the number is what separates them from the 73% who haven’t.

The single most predictive variable in the entire dataset is comfort level. 0% of those who described themselves as very uncomfortable with in-platform purchasing have ever bought in-platform. Not one.

Comfort level functions less like a sliding scale and more like a threshold that purchase behavior follows.

One purchase changes almost everything

The attitudinal gap between those who’ve bought in-platform and those who haven’t is striking (and it runs across every question in the survey). Those who’ve bought are significantly more positive about every platform, including ones they haven’t purchased on.

0% of people who have bought in-platform are very negative about Google, ChatGPT, or social media shopping. Among non-buyers, very negative responses range from 25% to 53% depending on the platform.

Trust gaps narrow quite a lot, too.

72% of those who haven’t bought in-platform trust brand websites significantly more than platforms. Among those who have, that drops to 23%. The act of buying in-platform doesn’t eliminate brand website preference, but it compresses the trust gap considerably.

Two completely different conversations

Those who’ve bought in-platform and those who haven’t don’t just have different attitudes. They want completely different things, which makes them almost impossible to address with a single marketing message.

Those who’ve bought want:

- Better prices (62%)

- Faster checkout (46%)

- Personalisation (31%)

They’ve cleared the trust barrier and are focused on improving the experience.

Those who haven’t want:

- Payment security (53%)

- Easy returns (44%)

- Proof the brand and products are legitimate (39%)

They haven’t decided whether to engage with the experience at all.

What this really reflects is two groups at completely different stages of trust. One has resolved the question of whether to engage. The other hasn’t. Meeting them where they are means understanding which questions and concerns influence their buying behaviors online.

Three Patterns That Emerge When You Look Across the Whole Dataset

Individual segments tell their own stories. But when you step back and look across age, gender, tech level, and purchase history together, three signals keep coming up.

Awareness doesn’t drive adoption, but experience does

40 out of 49 respondents knew in-platform shopping existed. Only 13 have ever done it. Awareness is very high in this sample, and it wasn’t enough to move the needle on purchasing.

What moves the needle is having tried it at least once. Shoppers who have made even a single in-platform purchase show dramatically different attitudes across all survey questions.

They’re more open, less distrustful, and less emotionally attached to the direct channel. The first purchase isn’t just a transaction. It appears to be the thing that unlocks everything that follows.

The more you know, the more fixed your position

This pattern emerges when we explore the data through the lenses of tech savviness, gender, and age simultaneously.

Very tech-savvy shoppers, 35–44 year olds, and men who haven’t purchased within a platform are all groups where deeper knowledge of how platforms operate correlates with stronger, more fixed resistance.

Knowledge doesn’t produce cautious curiosity. It produces conviction, often against shopping within such platforms and generally preferring marketplaces like Amazon instead.

Men and women are shopping in parallel universes

The gender gap is the most consistent finding in the entire dataset.

Different default channels, different gateway platforms, different concerns, and different conversion levers.

Men and women don’t just have different purchase rates, they have fundamentally different experiences of online shopping. Any platform or brand strategy that treats them as a single audience is likely missing both.

What This All Adds Up To

The resistance to in-platform shopping captured in this data is remarkably well-informed, given the predominantly tech-savvy group of survey participants. And that makes it a harder problem to solve than a UX update or a better price point can fix.

The practical barriers are real and addressable. But the credibility barriers are not (at least not quickly). Platforms have behaved in exactly the ways that have led many informed shoppers to distrust them for many years.

Past experiences with scams, dodgy purchases, or inadequate post-sales support shape significant distrust toward emerging ecommerce experiences. The people who understand that best are the least likely to convert.

Perhaps the most underrated finding, however, is that one purchase within a platform has the power to radically change a shopper’s attitude and future purchase decisions.