If a new business is a home, the business structure is its foundation. No matter how savvy a business owner you might be, the wrong structure choice can shut your startup down fast. Should you start a pass-through organization or a sole proprietorship? Can you register as an S corp in your state?

The answers to these questions will impact operations, taxes, and overall risk. Whether you’re building an early business plan or preparing a business for growth, this guide to business structure will give you the information you need to create a sound structure for your startup.

Why Business Structure Is So Important

The business structure is the foundation for the entire business, and the decisions you make in its earliest days guide its future. Most businesses will need a structure before registering with the state. Digital nomads have even more to consider. Whether you operate your business from your house or in different locations around the world, the tax and liability regulations of different countries and states will play a major role in business decision-making.

The wrong business structure can create tax complications, legal issues, or even dissolve your business involuntarily. So understanding the different kinds of business structures and choosing the right one for you is vital.

Let’s review some business structure basics. These are the most common business structures.

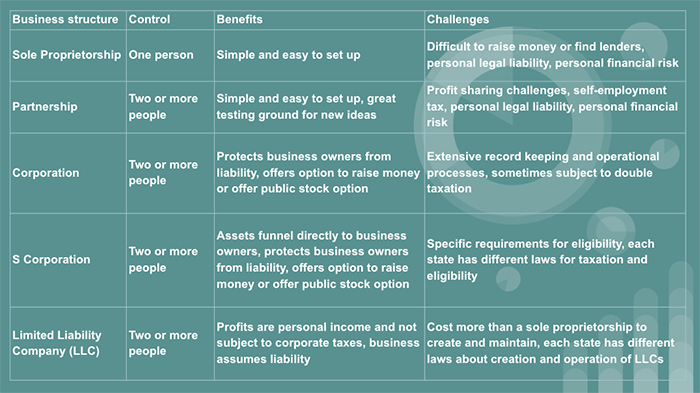

Sole proprietorship

Most small businesses are sole proprietorships–that is, run by just one person: you. This is the default business structure in most states. If you don’t choose a specific business structure your business will be a sole proprietorship.

Partnership

A partnership is a simple structure for two or more people to own a business together and is a good choice for professional groups.

Corporation or C corp

Corporations are legal entities separate from business owners. A C corp protects business owners from liability but they cost more to start and operate. C corps can continue doing business during major leadership and shareholder changes. They can also raise capital by selling stock. Most businesses that need to raise money, plan to offer a public stock option, or plan to sell the business at some future point are C corps.

S Corp

An S corporation avoids the sometimes double taxation of a C Corp and allows profits and some losses to go directly to the business owner.

Benefit corporation or B corp

B corps have the same financial structure as a C corp, but approach their organizational structure in a different way. B corps balance passion with profit. Besides operating a successful business, B corporations must produce a public benefit.

Non-profit corporations

Non-profits are often known as 501(c)(3)s because of their tax-exempt status. These corporations also do work for public benefit.

They often include the following types of business:

- Charities

- Schools and other educational organizations

- Religious organizations

- Orgs for the arts and sciences

Limited Liability Company or LLC

This business structure is a blend of corporate and partnership business structures. An LLC protects the business owner’s personal assets from liability and they often enjoy lower tax rates. This business structure is a popular choice for startups.

A quick important note

Sole proprietorships and partnerships are sometimes called informal business structures because there is no legal separation between the business and its owners.

Corporations and LLCs are formal business structures because the businesses are legally and financially separate from their owners.

Quick Tips To Improve Your Business Structure Today

Many of the decisions around the business structure are deep dives into the future of the business. But there are a few quick and simple decisions you can quickly make that will give you a sense of which business structure is right for your business.

1. Know the tax differences between business structures

Business structure determines the type of taxes a business needs to file. Choosing the right business structure can save a business owner 10%-40% in taxes each year!

Start researching local and other state tax laws to get a better understanding of your options. Ask yourself:

- What kind of protection will you need?

- What will your taxes look like?

- What are the legal risks of your product?

For example, C corps are common for businesses that plan to scale in a big way. At the same time, double taxation is a common concern for business owners running C corporations. Governments tax corporations for profit each year. The government also taxes shareholders when the corporation distributes profits as dividends. To avoid this double taxation, pass-through structures like LLCs and S corps are increasing every year.

It’s a good idea to speak to a tax professional or financial planner if you’re not sure whether a change to your business could help save money at tax time. If you don’t feel ready for this conversation yet, install accounting software early. This will keep your records in order and help a professional quickly assess the best financial plan for your business when it’s time.

2. Make sure your personal assets are protected

A college student running a business has a different outlook on assets than a business owner with a family of four. Owning a house, several cars, and other big-ticket items are signals of success for business owners. They’re also assets that a sole proprietorship or partnership won’t protect.

A few hot items in ecommerce over the last few years include candles, beard oil, and scented lotions. These DIY creations are an incredible way to start a business and quickly make a profit. They also leave business owners open to lawsuits for severe allergic reactions, accidental fires, and more.

Most businesses will need to worry about a lawsuit at some point. While formal business structures are more complicated to launch, they also offer more protection. If you’re not sure which business structure is best for your business from a liability perspective, speaking to a legal professional is the right next step.

3. Understand your income sources

Most small businesses shut down because of funding issues. Business structure has a dramatic direct impact on your access and ability to raise money for the business.

No matter how solid a business budget is, surprise changes in healthcare legislation, local politics, or on-the-job accidents can flip a budget in no time. As demand for your product grows or shifts, access to other sources of capital may be out of reach if you don’t choose the right business structure.

If you are thinking about these income streams take a close look at your options with each business structure.

- Bank loans

- Investor funding

- Selling public shares

Decide early on about what you expect your primary income streams to be, then calculate the future investment your business will need to make if you want to make changes later.

Long-Term Strategies for Business Structure

The business structure you choose sends a signal to potential customers and investors about your plans for the future. While running a sole proprietorship is the simplest way to go, it also can indicate that you are more interested in short-term profit than long-term growth.

These strategies will help you and your team think through the implications and benefits of each business structure.

1. Choose a long-term location

It is tempting to set up your business structure locally, but because many legal business structures and their regulations vary by state, it’s a good idea to make your businesses’ home the location that is most advantageous to your business

Before packing up and moving out, get to know the local politicians in the area. Set a Google alert to track regulations and other legal updates. This will give your business up-to-the-minute notice if changes to state and other local laws will have an impact on your business structure or operations.

2. Document your thought processes

The structure of the business is a decision that will have a wide-ranging impact, so don’t jump on the first impulse. Also, don’t choose a legal entity as the first step in the business plan. Instead, use the details in your initial business plan to guide business structure decisions.

The business structure validates the business and shows potential supporters how seriously you are taking this venture. As you make business structure decisions, on your own or with the team, carefully document and outline the thought process.

Don’t just take meeting notes. Create a formal outline that validates each decision as you write this document. Think about your ideal vision for the business in five to ten years. Begin with this future vision of the business and then work backward to where you are now. This process will help clarify your expectations for outside funding, the anticipated number of shareholders, and the scale of your dream team.

This kind of imaginative exercise can be tough for people who are more used to crunching numbers or project management. You might want to coordinate a team brainstorming session to expand on and validate early ideas.

3. Assemble the team you need

The process of selecting the right business structure often highlights the biggest challenges of starting a business. It can be a humbling experience that brings the weaknesses of even the strongest business owners front and center.

Hiring the right team often means selecting employees whose strengths balance your biggest challenges. To hire the best employees for your business, keep these challenges and insecurities top of mind.

For example, a solo business owner making 100 sales per month can easily track and fulfill customer orders. But when sales jump to 1000 orders per month, a business owner can become quickly overwhelmed, especially if the business structure requires their answer or opinion for every decision.

If that same business owner anticipates these challenges in advance they might hire an expert in maintenance operations to scale this part of the business. Another option is to budget for a computerized maintenance management system early on.

4. Consider your business succession plan

Running a new business is intense and busy. When a business begins the farthest some owners can project into the future is a few months. If owners don’t take dedicate time and thought to a succession plan, they may see their business fade away for reasons they never considered.

For example, two partners we know started a business in 2011, just after graduate school. Their business is still getting press and funding, but the owners are exhausted. They are ready to do something new, maybe start over in another location, but they don’t want to let the business they put so much into fall apart. They’re in a bind now because their entity structure doesn’t match their ideal succession plan.

The reasons business structure is important to a business also have a major impact on succession planning.

Business structure impacts the future above of a business because of the effects it has on:

- Business taxation

- Personal taxation

- The company’s ability to transfer capital

To prepare for succession, examine the pros and cons of each business structure. Next, bring different types of stakeholders into the discussion. These concerns are also important to address if you’re thinking about selling the business someday.

5. Consider changing the business structure later

Another option for bootstrapped businesses is to stick with a low-risk initial business structure. There is always an option to change the structure later on, when the business is thriving.

If you want to change your business structure, check with your state first. A change to entity structure can create a domino effect, initiating new filing fees and paperwork outside of the budget. A business may need to change company bylaws, operating agreements, and other legally binding forms. It’s also a good idea to investigate the effect a structure change could have on your insurance, vendor requirements, taxes, and liability.

Next Steps

Establishing a legal entity helps new business owners prepare for the financial and legal obligations of any company. Business structures are also the ways a new business owner organizes and manages their staff and supply chain.

Entrepreneurial structures are often informal, and the owner tends to make most big decisions. Many corporations are also called bureaucracies. This structure tends to resemble a machine with precise standards and repetitive processes. As you consider the structure of your business, don’t forget to put a management plan in place. Then select management software and other tools that support the structure to enable your business to flourish.