Disclosure: This content is reader-supported, which means if you click on some of our links that we may earn a commission.

You may be the owner of a registered business, an ecommerce seller, or a freelancer. In the eyes of the law, however, you’re simply self-employed.

Filing taxes as a self-employed worker is slightly more complicated than filing one as a W-2 employee. You don’t have an HR department to calculate the taxable figure for you. Nor do you have a payroll team to deduct the right amount from your paycheck. Satisfying the IRS is solely your responsibility.

This Crazy Egg guide will tell you everything you need to know about self-employment taxes, including why it’s important, how to calculate it correctly, and what you can do to save on tax money.

Why Are Self-Employment Taxes So Important?

Self-employment taxes are the imposed taxes small business owners must pay to the federal government to fund Medicare and Social Security. These are similar to the FICA taxes paid by an employer.

Every United States citizen has to pay tax on their income. Since W-2 employees have their income tax withheld directly from their paychecks, they never really see that money entering into their account—it goes straight to the government.

On the other hand, when you’re self-employed, it’s likely your income isn’t taxed when you receive it. You may be paying yourself upfront without withholding any amount, meaning you’ll have to pay all the taxes on your income after receiving it.

What’s more, W-2 employees also have Social Security and Medicare taken out from their paychecks. Naturally, you have to help shoulder the load too by paying from your self-employment income, which is the part we call self-employment taxes.

If you don’t file your self-employment taxes and you earn more than $400 in profit during the year, you‘ll find yourself on the wrong side of the law. Many things can happen, but none of them will be good.

Take Robert T. Brockman’s case, for instance.

On October 15, 2020, Brockman, CEO of a multi-billion dollar company, was indicted in a 20-year scheme to hide $2 billion in income. With several serious charges against him, Brockman potentially faces a substantial period of incarceration, criminal forfeiture, and restitution.

To put things into perspective, here’s what happens if you don’t pay your self-employed taxes:

- The IRS will prepare the tax return for you, sans any tax benefits. You’ll end up paying a lot more than you would’ve had you filed the return yourself.

- The IRS will levy heavy penalties on you starting at 5% per month on the amount of taxes you owe to a maximum of 25% after five months.

- The IRS can take your entire self-employment income to pay back taxes.

- Delay in filing tax returns can lower your future Social Security benefits.

- You may face difficulty when applying for personal or financial loans.

Therefore, make sure you file your return on time and avoid owing the IRS any money in the future. Set aside the necessary funds and start making estimated tax payments.

Quick Tips to Improve Filing Self-Employment Tax Returns

Below, we’ve compiled a list of tips you can use to make your life easier when filing self-employment taxes without getting on the wrong side of the IRS.

Keep Up With the Self-Employment Tax Rates

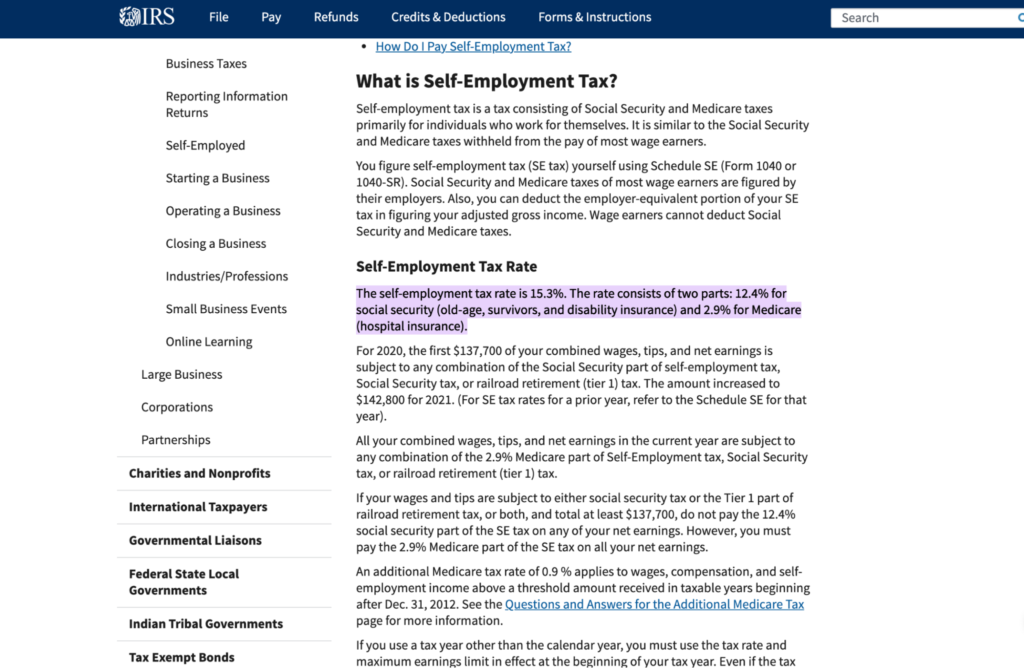

Currently, the self-employment tax rate is 15.3%—2.4% for Social Security and 2.9% for Medicare. Things aren’t this black and white, though. The splitting of your self-employment tax is for a reason.

The tax you pay on the Social Security is capped based on your earnings, with the thresholds subject to change each year. For instance, in 2020, the first $137,700 of a self-employed individual‘s wages, tips, and net earnings was subject to the 12.4% employment tax rate for Social Security. In 2021, this increased to $142,800.

On the other hand, the treatment for the 2.9% for Medicare is very different. First, there is no cap. Second, if your net earnings cross the $200,000 mark (and you’re single), you’ll have to pay an additional 0.8% for the Medicare potion, bringing your total Medicaid tax rate to 3.7%.

Track Your Business Expenses Carefully

When you’re self-employed, you’ve got a lot going on. Keeping track of all your business expenses takes a back seat, making it harder to file accurate tax returns.

But you should certainly take the initiative of tracking all your expenses from the beginning of the financial year.

Unlike tax deductions, business expenses affect your net income. So when you lower your income, the amount you owe in taxes also reduces. For instance, if you buy new office furniture, you can get the amount you spent taken off from your income.

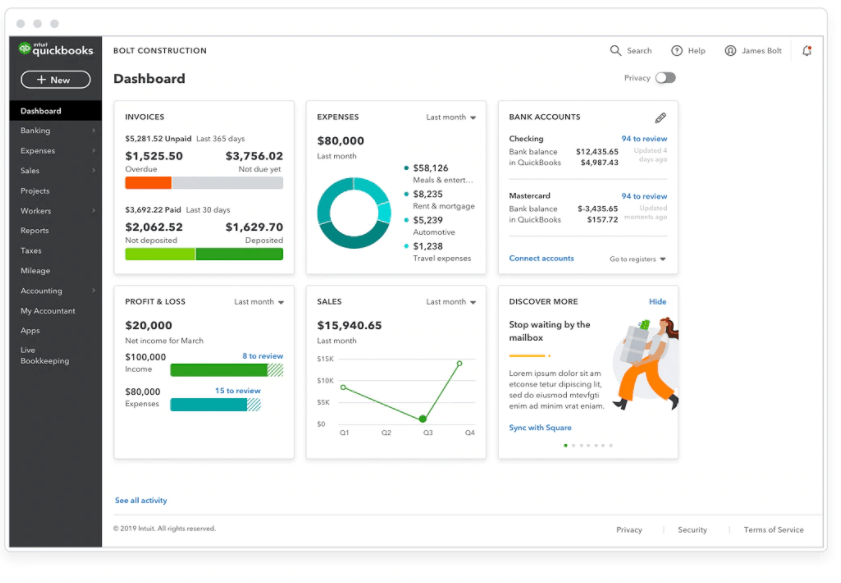

We highly recommend using reliable accounting software to track your business expenses carefully. Eliminating any manual work to keep track of paper receipts will not only save time, but it’ll make the whole expense tracking process less tedious, too.

QuickBooks, for one, offers excellent accounting solutions for self-employed individuals. Sync it with your bank account and credit card to auto-track business transactions.

You can also take pictures of store receipts using the QuickBooks app, after which the software will auto-match them to your business expenses. Simple, secure, and convenient.

Hire a Good Accountant

A common mistake most self-employed entrepreneurs make is trying to do their own accounting. It’s their attempt at saving a few hundred dollars every year.

What they don’t realize is an accountant does so much more than managing your finances.

Accountants can give you reliable tax advice, helping you reduce your self-employment tax, and help you file your self-employment taxes properly.

The IRS has several rules and stipulations for different scenarios, which makes self-employment taxes slightly harder to follow for individuals who aren’t accounting experts. You’ll probably find yourself spending hours trying to get the calculations right if you don’t speak accounting.

Plus, as an entrepreneur, your time is your greatest resource. Make sure you save it and hire a good accountant to look after your account and file tax returns.

Opt for Estimated Quarterly Tax Payments

The IRS allows you to make quarterly tax payments if you expect to owe $1,000 or more in taxes when filing tax returns. You can either pay your total estimated tax bill on April 15 or split it into four equal amounts. If you choose the latter option, you have to be aware of the due dates, which are:

- 1st payment – April 15

- 2nd payment – June 17

- 3rd payment – September 16

- 4th payment – January 15

Paying taxes in small amounts will help keep your cash flow steady as opposed to paying a large amount at once.

Depending on your location, you might also owe estimated quarterly payments to your state’s office.

While we’ve used the word “estimated,“ you should ensure the figures are as accurate as they can be to avoid under-withholding. Not paying enough in quarterly payments may result in you getting penalized by the IRS.

Save 25% of Your Self-Employed Income for Tax Payments

Managing tax obligations isn’t easy.

You have to figure out how much you actually make after taxes for every financial year. Besides, your final tax figures, including self-employment taxes, will always vary based on your net income, deductions, expenses, credits, filing status, and several other factors.

Luckily, things won’t be as complicated if you follow a simple rule: set aside at least 25% of your earnings for tax purposes. That’s it.

You can either take 25% of the amount every time you get paid by your client and put it in a separate account or do it monthly after calculating your total income. This way, you won’t have to worry about having insufficient cash to pay your taxes.

Long-Term Strategies to Reduce Self-Employment Taxes

Paying the entire self-employment tax owed can be difficult. After all, it’s over 15% of your income. The good news is you can reduce this amount legally.

File Your Taxes With 1040

Any individual earning $400 or higher in self-employment income must file a tax return. The return must include a Schedule SE, which is a common tax form used to calculate the tax owed.

But when you file your taxes using 1040, you can avail yourself of a deduction—counting your self-employment tax payments as an adjustment to income.

Depending on how much self-employment income you earn, you can deduct between 50% to 57% of your self-employment tax payments. Having an accountant will definitely come in handy at this point.

Opt for an S-Corp Election

LLC (Limited Liability Company) or corporation owners can reduce their self-employment tax burden by electing to have their business taxed like an S Corporation or S-Corp.

With an S-Corp, you can pay yourself a reasonable salary out of earnings, as well as distribute any remaining profits to yourself or any other shareholders or partners. You can also leave the money in the business if you want. In certain situations, the money in excess of your salary is subject to income tax but not employment taxes.

For more context, an S-Corp owner only pays Social Security and Medicare taxes on their salary, whereas LLC owners have to pay self-employment taxes on 100% of their share of the LLC‘s profits.

That said, making an S-Corp election may not be best for your business. Talk to a tax or business formation professional before making a switch.

Reduce Overall Net Profit

Schedule C is necessary to calculate your net profit from self-employment. You must include this as income on your 1040 and on Schedule SE to calculate your self-employment tax.

Your net profit will equal the gross receipts you earned minus your deductible business expenses. So, the lower your net profit number, the lower your employment tax bill.

If you want to reduce your self-employment tax, you have to be thorough when preparing your Schedule C. Ensure you deduct every possible business expense, including office rent, telephone bill, office supplies, equipment, and business vehicle acquisition and maintenance costs, among other expenses.

Remember, your business expenses must be ordinary and necessary to operate your business to be deductible—they cannot be personal.

Next Steps

Now that you have a fair idea about your taxes, the next step is to ensure you take measures to keep track of your business expenses. This will help you make accurate tax estimates for making quarterly payments and take advantage of deductions to lower your overall tax amount.

We strongly recommend getting an accounting software tool to get your finances in order. Another good tip is to create a business bank account to separate your personal finances from your business finances.

Check out the following Crazy Egg guides to choose the best accounting software and business checking account for your enterprise: