We know about the challenges associated with finding funding for a small business, especially when you may not want a hard credit inquiry to affect your credit score. Fortunately, we’ve found options for loans that do not require a credit check, giving you the funds you need to move things forward. Fundbox is the best no-credit-check loan for most small businesses, as it requires the fewest hurdles to jump through to secure funding.

The Best Small Business Loans with No Credit Check for Most

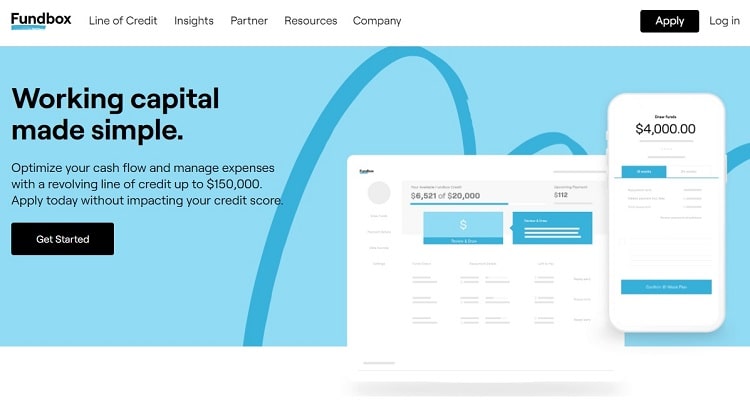

Fundbox

Best for Most

Fundbox bases your loan request on your business’ invoicing and revenue history, which makes it less restrictive than other options. This means you don’t go through a hard credit inquiry, which can be a big benefit.

Many small business loans that don’t rely on a credit check require you to use another service that the lender offers. With Fundbox, however, you don’t have to sign up for a credit card or use some service offering, which is why we selected it as the best option for most small businesses.

Fundbox simply needs to see proof of your invoicing history. Ideally, Fundbox wants you to provide several months of invoicing and revenue history, but they can work with what records you have. Fundbox also gives you multiple options for borrowing and repayment. That flexibility is another reason why we like it for many different kinds of small businesses.

The Best Small Business Loans with No Credit Check Options to Consider

- Fundbox – Best for most

- PayPal Working Capital – Best for PayPal Business account holders

- Square Capital – Best for businesses that use Square POS

- Shopify Capital – Best for businesses that sell with Shopify

- American Express Business Loan – Best for AmEx Business card holders

- Kiva – Best for crowdsourced loans

When It Makes Sense to Invest In Small Business Loans with No Credit Check

Startup costs for businesses and ongoing costs can be a huge challenge. Ideally, your small business will have perfect credit and a solid history of income generation. In that scenario, lenders are lining up to offer you loans when you need them.

In the real world, however, that isn’t always the case. Especially early on. When you don’t have a detailed business credit history and your personal credit score may not be as strong as you’d like, obtaining a loan can represent a significant uphill climb.

If you are struggling to obtain a small business loan through traditional means, seeking a small business loan without a credit check may be a good route for you to try.

It’s important to understand that these lenders are not going to just lend you money without a high degree of certainty that you will be able to pay it back. The best way to use a no-credit-check business loan is when you have a history of successful sales and invoicing in your business. You may not need several years of history, but most lenders want to see at least several months of sales in the books.

For new businesses seeking seed money, startup business loans are probably a better option than a business loan with no credit check. If you don’t qualify for startup loans, there are ways to start a business with no money that may give you the ability to get off the ground.

Once you are up and running for a few months, though, seeking a small business loan that doesn’t require a hard credit inquiry then may be a workable option.

#1 – Fundbox – Best for Most

Fundbox

Best for Most

Fundbox bases your loan request on your business’ invoicing and revenue history, which makes it less restrictive than other options. This means you don’t go through a hard credit inquiry, which can be a big benefit.

Fundbox does not have as many restrictions as other lenders of small business loans. You can receive an answer about your loan request within a few minutes and all you have to do to apply is fill out a simple form and connect your business banking account. If approved, you can receive the money the next business day.

Even if you have a lower credit score than average, you may still qualify for a Fundbox loan. In determining creditworthiness, Fundbox places more of an emphasis on your business’ current invoicing and income versus looking primarily at your credit score.

Fundbox prefers lending to businesses that have at least $100,000 in annual revenue or that are on track over several months to reach $100,000 in annual revenue.

Fundbox offers a business line of credit up to $150,000. However, the actual amount you can obtain and the interest rate you will pay depends on your creditworthiness. When you are ready to withdraw funds against your line of credit, you can select the repayment term from options up to 52 weeks. Their portal will show you your exact interest rate when you are ready to withdraw the money against the line of credit.

Secure a line of credit based on your invoice and income quality through Fundbox today.

#2 – PayPal Working Capital – Best for PayPal Business Account Holders

PayPal

Best for PayPal Business Account Holders

PayPal Working Capital is a popular option for small business loans that don’t require a credit check because the application process goes fast. However, you must be a PayPal seller to use it.

PayPal Working Capital is a very popular option for a variety of small business owners. Consequently, we almost made it the top selection on this list. However, the main reason it didn’t take the top spot is because it’s only available to those who have been accepting sales payments through PayPal for a while.

PayPal Working Capital won’t allow you to sign up with PayPal then immediately apply for a loan because they want to measure your projected annual sales for several months before offering you funding.

Only businesses that are PayPal Business or Premier account holders and who do at least $15,000 in annual sales through PayPal are eligible to apply for a loan through PayPal Working Capital. That being said, those who qualify get a solid loan with no credit check required.

PayPal offers loans for up to one-third of your annual sales, with a maximum of $125,000 for new borrowers. Once you pay back a few loans, your maximum borrowing amount increases to $200,000.

Paying back the loans is easy, as PayPal Working Capital takes a percentage of your PayPal sales over a period of up to 18 months as payment.

#3 – Square Capital – Best for Businesses That Use Square POS

Square Capital

Best for Businesses That Use Square POS

If you already use Square for your point of sale business transactions, this is one of the best no-credit-check loan options. Square’s interest rates are competitive too.

You’re likely noticing a pattern here. Once again, Square Capital is only available to those small businesses who already sell through Square’s point of sale platform, so it is not a good choice for everyone. However, it also is one of the easiest business loans to obtain without a credit check.

Square Capital requires that you have a healthy business, which it will check based on the transactions you are running through Square. But its minimum of $10,000 in annual sales to apply is one of the lowest requirements we’ve seen.

Depending on your sales, you can obtain a loan of up to $250,000 through Square Capital with up to 18 months to repay it.

As a bit of an oddity, you don’t actually apply for a Square Capital loan. Square will potentially make loan offers to you, but you cannot control when such offers will appear. You can click a link inside your account to see if Square Capital has any loan offers available for you, just be vigilant to accept the offers when they’re made available to you.

Learn more about Square Capital loans to learn if this option fits your needs.

#4 – Shopify Capital – Best for Businesses That Sell with Shopify

Shopify Capital

Best for Businesses That Sell with Shopify

If you run your online business through Shopify, you could qualify for a small business loan. These loans can be large for those who have a significant volume of sales.

While most of the lenders above are credit card companies or payment processors, the leading ecommerce platform also has an offering for small businesses using their platform. With Shopify Capital, Shopify users may be eligible to obtain a loan.

As with Square Capital, though, you do not apply for Shopify Capital loans. Instead, if Shopify decides you qualify, it will make loan offers to you.

The loan amount you could receive will depend on your sales volume through Shopify and on the type of business you are operating.

You can have up to 12 months to repay your loan, and Shopify Capital will pull repayments out of your daily sales through Shopify, making it easy to repay what you borrow.

And Shopify is generous with its lending limits. You could qualify for up to $2 million if you perform a significant enough amount of sales through Shopify.

Learn more about funding your Shopify business with a Shopify Capital loan.

#5 – American Express Business Loan – Best for AmEx Business Card Holders

American Express Business Loan

Best for AmEx Business Card Holders

For those who hold an American Express Business card, this loan is a great option when your income stream is a little slow. But you will need at least two years of business history to qualify.

Although an American Express Business Loan is pretty easy to obtain for those who qualify, it does have quite a few restrictions associated with it. Like with the PayPal option above, AmEx only offers these loans to holders of their Business credit cards. You will need to have 24 months of business history and at least $200,000 per year in sales to apply.

Additionally, this type of loan only works to pay off your vendors when your cash flow is slow. These funds are not usable for just any expense you have. American Express sends the funds directly to your vendors. But since this loan can cover those expenses for a stretch of time, it still frees up the rest of your funds for other uses.

You can obtain up to $75,000 in a loan with a potential payback period of up to 36 months. See what you can secure with your American Express Business credit card today.

#6 – Kiva – Best for Crowdsourced Loans

Kiva

Best for Crowdsourced Loans

If you don’t want to take out a traditional type of small business loan, Kiva is a strong alternative. It uses crowdsourcing to help businesses receive small loans.

Kiva is a unique platform for securing a loan. It uses the idea of crowdsourcing to help small businesses seek funding without having to go through a traditional credit check.

This platform relies on peer-to-peer lending, with willing investors signing up for the platform to lend as little as $25 to as much as they are comfortable with. Once the funds are raised and given to the borrower, the recipient of the funding pays back the loan over time. The individual lenders get their money back to fund other loans, donate, or withdraw.

If you can convince investors on Kiva about the viability of your business and the need for the loan, you could receive a no-interest loan of up to $15,000 with a repayment time of up to 36 months. That’s a great rate for small-scale funding.

Unfortunately, Kiva’s maximum loan amounts are extremely small. Businesses less than three months old have a $5,000 cap. Additionally, you will have to come to Kiva with some proven funding commitments from other investors or friends and family members before Kiva will accept and underwrite your loan request.

Explore this unique platform for crowdfunding a small business loan. Sign up on Kiva and get the best rates on a small business loan with no credit check.

Methodology for Choosing the Best Small Business Loans With No Credit Check

When we studied the market for the best lenders who provide small business loans without requiring a hard credit inquiry, we focused on the following important criteria.

Type of Loan

As you are seeking funding, you may know that you need a certain amount as soon as possible. In a case like this, a traditional term loan that you will repay over a certain amount of time will be a desirable option.

However, if you need funding here and there for different items, but you can’t really predict the amount you will need or exactly when you will need it, a business line of credit may be better.

Think about whether you need one type of loan versus the other. If so, seek a lender that focuses on the area that you need.

Interest Rates

As you might expect, when you seek a small business loan without a credit check, you’re going to pay a higher interest rate than when using a traditional loan option. Unfortunately, this is part of the trade-off for seeking a no-credit-check loan.

However, you still can shop around to find different interest rates. You may even be able to reduce your interest rate by agreeing to certain terms for the loan, such as automatic bank withdrawal or a shorter borrowing period.

In other words, don’t let the fear of a significant interest rate cause you to completely avoid this type of loan. Instead, look into ways you may be able to reduce your interest rate with different lenders.

Are You Already Using the Lender’s Services?

Another major restriction on small business loans without a credit check is that they’re usually only available to customers of another product or service the lender offers. You’ll see above that four of the six top picks come from a credit card company, an ecommerce platform provider, and two payment processing companies.

Not only do you need to use another of their offerings, but you’ll need a history with them, too, to apply. With PayPal, American Express, Square, and Shopify, they’re going to look at your company’s revenue history and financial health before extending a loan offer.

If time is of the essence and you’re not already offered credit check-free loans from another company servicing your business, you’ll need to look to options like Fundbox or Kiva.

Credit Score Still Matters

Even though these lenders offer loans without making a hard credit inquiry, your credit score still may play a role in acquiring the loan.

Some lenders will request a soft credit inquiry for this type of loan to review your credit report without telling the credit bureau that you are requesting a new line of credit or a loan. It doesn’t affect your credit score, but it can definitely affect their lending decision, from the maximum amount you can borrow to the interest rate. With an especially low credit score, you may not qualify for the loan, even though a hard check wasn’t made.

The good news is that most of these lenders will not make a determination on whether you receive the loan based solely on your credit score and may rely more on your revenue history for their decision. If you have an affiliation with the lender already, such as using it for POS, this reduces your credit score’s importance.

Some small business lenders may consider your personal credit score if your business doesn’t have a credit score yet. Some lenders may consider both credit scores together.

Fundbox

Best for Most

Fundbox bases your loan request on your business’ invoicing and revenue history, which makes it less restrictive than other options. This means you don’t go through a hard credit inquiry, which can be a big benefit.

The Top Small Business Loans with No Credit Check in Summary

Obtaining a business loan that requires a hard credit check may not be the ideal situation for you. In those cases, seeking a loan that does not require a credit check is the best option for funding your growing business.

We recommend Fundbox for the majority of small business owners in this situation, as it has fewer limitations for obtaining funding than other options. However, if your business fits under one of the specific criteria mentioned for the other lenders on our list, one of those lenders may give you better results.